How much house you can afford in Northern Virginia depends on your household income, your down payment, current interest rates, and which county you're looking in. A household earning $170,000 per year can typically afford a home around $600,000 with 20% down at today's rates, while a $250,000 income opens the door to homes in the $800,000 to $900,000 range. But the real answer shifts depending on where in Northern Virginia you're buying: a $600,000 budget puts you below the median in Fairfax and Loudoun counties but comfortably in range in Prince William County.

At ML Real Estate Group, we help 160 to 170 families buy and sell homes across Northern Virginia every year, with an average sale price above $650,000. We work with buyers at every price point, from first-time purchasers in Gainesville and Haymarket to move-up buyers in Fairfax, Reston, and Loudoun County. The most common mistake we see is people asking whether they can afford "Northern Virginia" when they should be asking which part of Northern Virginia fits their budget.

This guide breaks down the actual math: what income you need, what your monthly payment will look like, how prices vary by county, and which loan programs and assistance options can stretch your buying power further.

These numbers assume the 28% front-end ratio, which is a guideline, not a hard cap. Some lenders will approve higher ratios depending on your overall debt, credit score, and cash reserves. But this table gives you a realistic starting point for what's comfortable rather than what's technically possible.

If you're putting less than 20% down, you'll need private mortgage insurance (PMI), which adds roughly $200 to $300 per month on a $600,000 home and pushes the income requirement higher. More on that below.

A couple things worth noting here. Property taxes are a bigger factor than most people expect. On a $750,000 home in Fairfax County, you're paying $700 per month in property taxes alone. And these numbers change depending on which county you buy in. Loudoun County's lower tax rate saves you roughly $200 per month on a $750,000 home compared to Fairfax.

If you put down only 10% instead of 20%, add PMI of approximately $225 per month on a $600,000 home (roughly 0.5% of the loan balance annually). That pushes your total monthly cost from $3,919 to over $4,400.

Use our affordability calculator to plug in your specific income, down payment, and debt for a personalized estimate.

These are medians, meaning half of homes sell above and half sell below. The range within each county can be wide. In Fairfax County, for example, the average single-family home sold for approximately $1.28 million in April 2026, while the average townhome was around $566,000 and the average condo was about $415,000. Property type matters as much as location.

For buyers with a budget under $600,000, Prince William County communities like Gainesville and Haymarket offer more home for the money. If your budget is in the $700,000 to $900,000 range, you'll find strong options across Fairfax County, much of Loudoun County, and pockets of Arlington (primarily condos and townhomes). Above $900,000, single-family homes in areas like Reston, Ashburn, and parts of Centreville become available.

One detail that surprises a lot of buyers: Northern Virginia's conforming loan limit for 2026 is $1,249,125, not the national baseline of $832,750. Because the DC metro area is classified as a high-cost zone by the Federal Housing Finance Agency, most homes here qualify for conforming loans with lower rates and smaller down payments. You don't need a jumbo loan unless you're buying above $1.25 million.

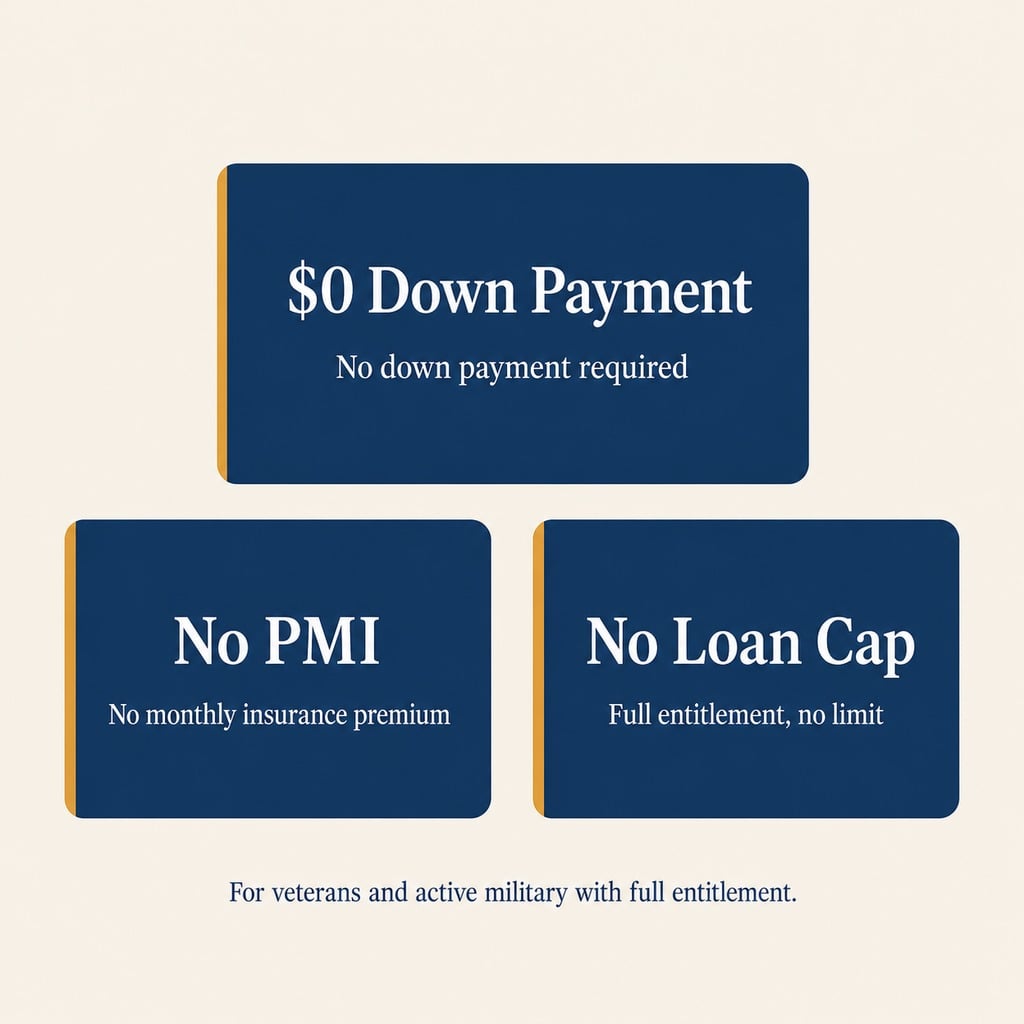

For VA-eligible buyers, this is one of the best markets in the country to use your benefit. VA loans have no down payment requirement, no PMI, and no loan cap for borrowers with full entitlement. Given Northern Virginia's proximity to military installations and federal agencies, many buyers in this area qualify for VA financing without realizing it.

For VA-eligible buyers, this is one of the best markets in the country to use your benefit. VA loans have no down payment requirement, no PMI, and no loan cap for borrowers with full entitlement. Given Northern Virginia's proximity to military installations and federal agencies, many buyers in this area qualify for VA financing without realizing it.

FHA loans also carry the $1,249,125 limit in all Northern Virginia counties, making them a viable option even for homes in the $800,000 to $1 million range if your credit score or savings don't support a conventional loan.

FHA loans also carry the $1,249,125 limit in all Northern Virginia counties, making them a viable option even for homes in the $800,000 to $1 million range if your credit score or savings don't support a conventional loan.

PMI typically costs between 0.3% and 1% of the loan balance per year, depending on your credit score and down payment percentage. It falls off automatically once you reach 20% equity, either through payments or home value appreciation.

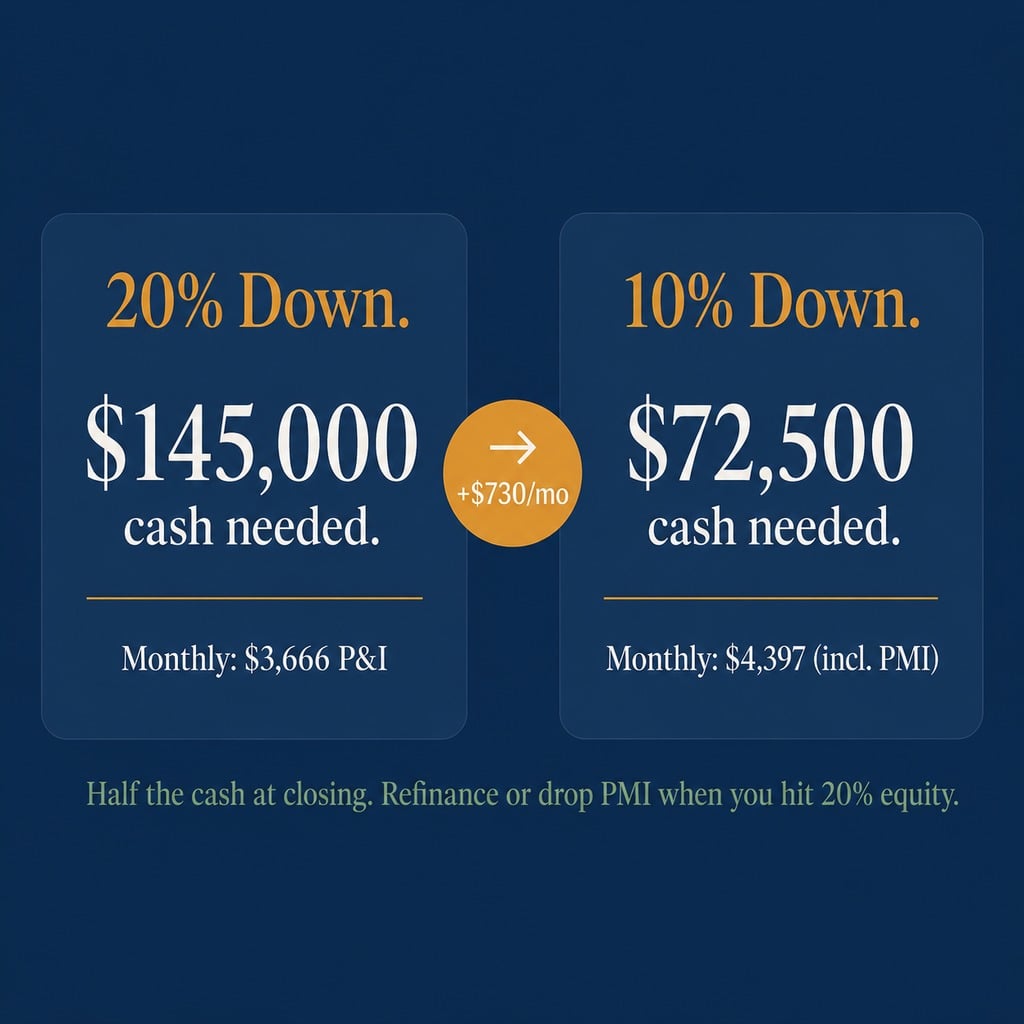

The trade-off is real but not as steep as many buyers assume. Going from 20% down to 10% down on a $725,000 home adds roughly $730 to your monthly payment (higher P&I plus PMI) but cuts the cash you need at closing in half. For a lot of buyers, that trade-off makes sense, especially in a market where renting a comparable home often costs $3,000 or more per month anyway.

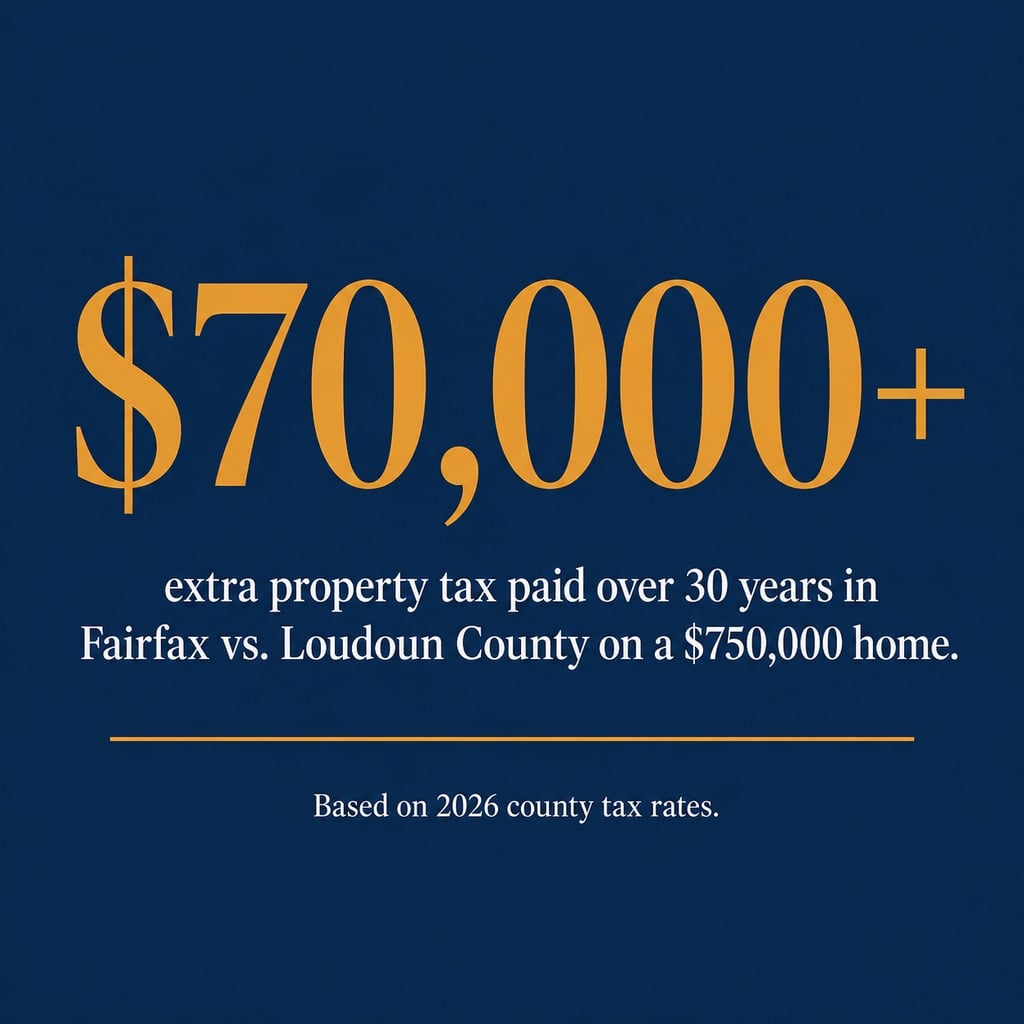

On a $750,000 home, buying in Loudoun County instead of Fairfax County saves you roughly $2,362 per year in property taxes, or about $197 per month. Over a 30-year mortgage, that difference adds up to more than $70,000.

This is why affordability calculations that use a single "Northern Virginia" tax rate can be misleading. The county you choose changes your effective housing cost by hundreds of dollars per month, and that difference should factor into your budget as much as the purchase price itself.

On a $750,000 home, buying in Loudoun County instead of Fairfax County saves you roughly $2,362 per year in property taxes, or about $197 per month. Over a 30-year mortgage, that difference adds up to more than $70,000.

This is why affordability calculations that use a single "Northern Virginia" tax rate can be misleading. The county you choose changes your effective housing cost by hundreds of dollars per month, and that difference should factor into your budget as much as the purchase price itself.

Buying at today's rates with less competition can mean a lower purchase price and a better negotiating position. That often makes up for the rate difference, and you keep the refinance option for later.

Buying at today's rates with less competition can mean a lower purchase price and a better negotiating position. That often makes up for the rate difference, and you keep the refinance option for later.

How Much Income Do You Need to Buy a Home in Northern Virginia?

The standard lending guideline is that your total monthly housing payment (mortgage principal, interest, property taxes, insurance, and HOA fees) should not exceed 28% of your gross monthly income. Using that rule with today's average 30-year fixed rate of roughly 6.5%, 20% down, Fairfax County's property tax rate, homeowner's insurance at approximately 0.35% of the home price, and a $150 monthly HOA, here's what each income level can afford:| Household Income | Approximate Home Price You Can Afford |

|---|---|

| $115,000 | $400,000 |

| $141,000 | $500,000 |

| $168,000 | $600,000 |

| $195,000 | $700,000 |

| $222,000 | $800,000 |

| $276,000 | $1,000,000 |

What a Northern Virginia Mortgage Actually Costs Each Month

The sticker price of a home only tells part of the story. Your actual monthly housing cost includes principal and interest, property taxes, homeowner's insurance, and often HOA fees. Here's what that looks like at three price points, all using a 30-year fixed rate at 6.5%, 20% down, Fairfax County's $1.12 per $100 tax rate, insurance at 0.35%, and a $150 HOA:| Monthly Cost Component | $600,000 Home | $750,000 Home | $900,000 Home |

|---|---|---|---|

| Principal & Interest | $3,034 | $3,792 | $4,551 |

| Property Tax | $560 | $700 | $840 |

| Homeowner's Insurance | $175 | $219 | $263 |

| HOA Fees | $150 | $150 | $150 |

| Total Monthly Payment | $3,919 | $4,861 | $5,804 |

Median Home Prices by County in Northern Virginia (2026)

"Northern Virginia" covers a wide range of price points. The county you choose is the single biggest factor in what your budget can buy. Here are the current median sale prices:| County/City | Median Home Price (2026) |

|---|---|

| Loudoun County | $805,000 |

| Arlington County | $729,000 |

| Fairfax County | $725,000 |

| City of Alexandria | $647,000 |

| Prince William County | $570,000 |

Which Loan Type Works Best in Northern Virginia?

The loan you choose affects your down payment, interest rate, monthly payment, and how much home you can afford. Here's how the main options compare in Northern Virginia's high-cost market:| Loan Type | Min. Down Payment | 2026 Rate (Approx.) | Max Loan in NoVA | PMI/Funding Fee | Best For |

|---|---|---|---|---|---|

| Conventional | 3% to 20% | 6.3% to 6.5% | $1,249,125 (conforming) | PMI if <20% down | Buyers with strong credit (700+) and savings |

| FHA | 3.5% | ~6.1% | $1,249,125 | Upfront + annual MIP | First-time buyers, credit scores 580+ |

| VA | 0% | ~5.96% | No cap (full entitlement) | Funding fee (can be financed) | Veterans and active military |

| Jumbo | 10% to 20% | Varies (often higher) | Above $1,249,125 | None (no PMI typically) | Luxury buyers above conforming limit |

For VA-eligible buyers, this is one of the best markets in the country to use your benefit. VA loans have no down payment requirement, no PMI, and no loan cap for borrowers with full entitlement. Given Northern Virginia's proximity to military installations and federal agencies, many buyers in this area qualify for VA financing without realizing it.

FHA loans also carry the $1,249,125 limit in all Northern Virginia counties, making them a viable option even for homes in the $800,000 to $1 million range if your credit score or savings don't support a conventional loan.

How Much Down Payment Do You Need?

The traditional 20% down payment is still the cleanest path because it eliminates PMI and gives you the lowest monthly payment. But requiring 20% on a $725,000 home (the Fairfax County median) means saving $145,000 in cash, which is a high bar for most buyers. Here's how different down payment levels affect a $725,000 purchase at 6.5%:| Down Payment | Cash Needed | Loan Amount | Monthly P&I | Estimated PMI | Total Monthly (P&I + PMI) |

|---|---|---|---|---|---|

| 20% ($145,000) | $145,000 | $580,000 | $3,666 | $0 | $3,666 |

| 10% ($72,500) | $72,500 | $652,500 | $4,125 | ~$272 | $4,397 |

| 5% ($36,250) | $36,250 | $688,750 | $4,354 | ~$287 | $4,641 |

| 3% ($21,750) | $21,750 | $703,250 | $4,446 | ~$293 | $4,739 |

Down Payment Assistance Programs in Northern Virginia

Several programs can help with the down payment, especially for first-time buyers: Virginia Housing (VHDA) Programs- DPA Grant: A 2% to 2.5% grant of the purchase price for first-time buyers using VHDA loans. On a $500,000 home, that's $10,000 to $12,500 you don't have to repay.

- Plus Second Mortgage: A second loan covering 3% to 5% of the purchase price, depending on your credit score.

- Closing Cost Assistance Grant: Up to 2% of the purchase price for buyers using VA or USDA loans, covering closing costs or the VA funding fee. This is a grant, so there's no repayment.

- Loudoun County DPCC Program: Offers forgivable loans up to 10% of the purchase price (maximum $70,000) for qualifying first-time buyers. Income limits apply (the eligible range is $49,200 to $114,749 regardless of household size).

- Fairfax County (FCRHA): Launched a program offering up to $50,000 in down payment assistance for first-time buyers earning 80% or less of the area median income. Funds are distributed on a first-come, first-served basis.

Why Property Taxes Change Your Affordability by County

Property taxes are one of the most overlooked factors in Northern Virginia home affordability. The difference between counties adds up to thousands of dollars per year on the same home price.| County/City | Tax Rate per $100 of Assessed Value | Annual Tax on a $750,000 Home | Monthly Tax Cost |

|---|---|---|---|

| Loudoun County | $0.805 | $6,038 | $503 |

| Prince William County | $0.906 | $6,795 | $566 |

| Arlington County | $1.033 | $7,748 | $646 |

| Fairfax County | $1.12 | $8,400 | $700 |

| City of Alexandria | $1.135 | $8,513 | $709 |

On a $750,000 home, buying in Loudoun County instead of Fairfax County saves you roughly $2,362 per year in property taxes, or about $197 per month. Over a 30-year mortgage, that difference adds up to more than $70,000.

This is why affordability calculations that use a single "Northern Virginia" tax rate can be misleading. The county you choose changes your effective housing cost by hundreds of dollars per month, and that difference should factor into your budget as much as the purchase price itself.

Should You Wait for Lower Interest Rates?

This is the question we hear most often right now. With 30-year fixed rates around 6.3% to 6.5%, some buyers are holding off, hoping rates come down before they buy. Here's our take, and it's the same thing our CEO Matt Leiva tells every buyer who asks: buy when it makes sense for you. Stop trying to time the market. Maybe rates drop another quarter point. Maybe they go up. Analysts have a range of forecasts for 2026. Fannie Mae projects rates could fall to approximately 5.7% by year-end. The Mortgage Bankers Association expects a more modest decline to around 6.1%. Nobody knows for sure. The key question is simpler than any forecast: what monthly payment makes this purchase work for you and your family? If that number works at today's rates, move forward. If rates drop later, you can refinance. You can always change your interest rate, but you can't go back and change the price you paid for the house. There's also a competition factor to think about. When rates drop, more buyers enter the market. That increased demand drives prices up and leads to bidding wars. The Northern Virginia market already has only about 1.8 months of housing supply, well below the six months considered balanced. Lower rates with the same tight inventory means more buyers fighting over the same homes.

Buying at today's rates with less competition can mean a lower purchase price and a better negotiating position. That often makes up for the rate difference, and you keep the refinance option for later.

How to Figure Out Your Personal Number

The tables and data above give you a framework, but your affordability number depends on your specific situation: income, existing debts, credit score, savings, and what loan programs you qualify for. Here's a practical sequence:- Start with the 28% rule. Take your gross monthly income and multiply by 0.28. That's your target maximum monthly housing payment including principal, interest, taxes, insurance, and HOA.

- Pick a county. Use the median price table above to see which areas match your budget range. Then factor in that county's specific tax rate.

- Choose a loan type. VA and FHA loans lower the barrier to entry. Conventional loans with 20% down give you the lowest monthly payment. The loan comparison table above can help you narrow this down.

- Check for assistance. If you're a first-time buyer, review the VHDA and county programs listed above. Even a 2% grant on a $600,000 home is $12,000 toward your down payment.

- Run your numbers. Use our affordability calculator to plug in your actual income, debts, and target area. The calculator accounts for current rates and local tax variations.

- Talk to a lender early. Pre-approval tells you exactly what you qualify for and locks your rate. We work with lenders across Northern Virginia who specialize in the local market and can walk through these numbers with you.

Ready to Find Out What You Can Afford?

Figuring out your Northern Virginia home budget is the first step. The next step is seeing what's actually available in your price range. We help buyers across Fairfax County, Loudoun County, Prince William County, and the wider DC metro area find homes that fit their budget and their life. Whether you're a first-time buyer looking at townhomes in Brambleton or a growing family searching for a single-family home in Clifton or Centreville, our team knows these neighborhoods and can help you make sense of the numbers. Browse current Northern Virginia listings or reach out for a free, no-obligation consultation. We'll go over your finances, walk through your options, and help you find the right home at the right price. Call us at (571) 357-0695 or email [email protected].Check out this article next